By Jeff Chan

October 2003

In order to encourage the use of Alternate Fuel Vehicles (AFVs), powered by Electricity, Natural Gas, and other relatively clean energy sources, in 1998 California enacted legislation to charge AFVs the Vehicle License Fees of the equivalent conventional vehicle. Mainly because large battery capacity is still very expensive, electric vehicles often cost 10-20 thousand dollars more than a gasoline vehicle they're based on, so the reduction in fees can be significant. What prompted many AFV owners to make this correction is that the fees doubled to tripled for most cars in 2003.

The legislation to charge AFVs registration fees of conventional vehicles is SB 1782 by State Senator Mike Thompson. Here's a local copy of chaptered (final) version of SB 1782, in HTML and PDF. And here is a press release by the California Energy Commission about SB 1782 (and a local copy). According to the press release and the text of the legislation as signed into law, the VLF reduction applies to AFVs purchased between January 1, 1999 and December 31, 2002.

According to the Department of Motor Vehicles' (DMV) Handbook for Dealers Completing New Vehicle Registrations Section 1.010 (local copy of AFV excerpt), it is the dealer's responsibility to prepare the Statement of Facts and other documentation to support this reduction, but many dealers, not familiar with selling AFVs, are ignorant of the details and fail to perform this duty. As a result, many owners of AFVs have found it necessary to do it themselves, or to find a dealer DMV clerk who knows what to do and is willing to help.

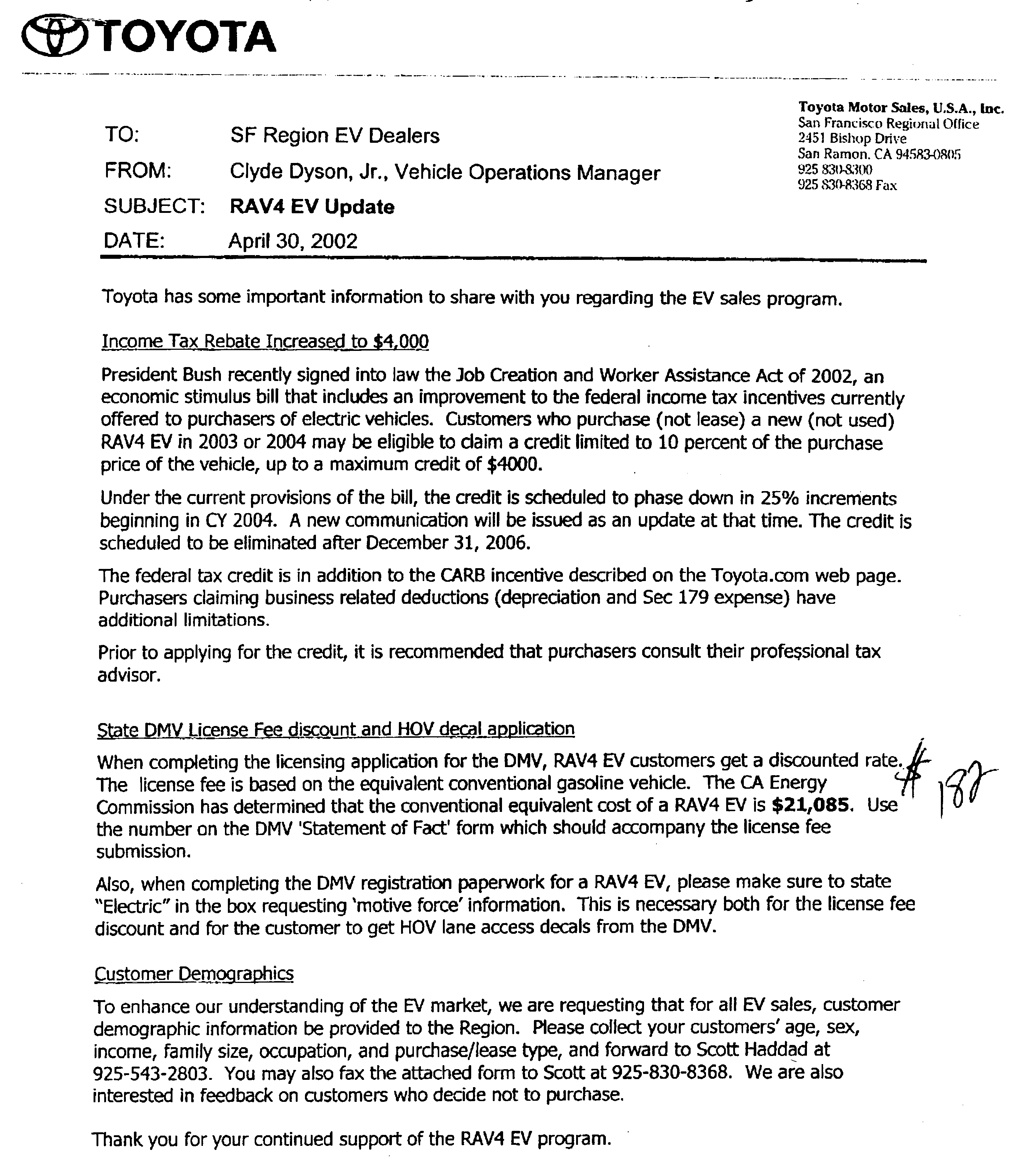

We tried to get two DMV clerks at our dealer, Stevens Creek Toyota, to help us with this, but they seemed incapable and unwilling to help, finally faxing back to me the information I faxed to them explaining what to do. We tried to get them to do their duty, but they seemed perfectly happy to foist it back onto us to do. That will certainly affect our perception of the willingness of that dealer to take care of their customers. (The information we faxed to them included this Memo from the Toyota Regional Office, Sample Statement of Facts Page 1 and Page 2 others have used to accomplish this, our registration statement, and a cover letter asking them to correct the registration fees and apply for a refund of last years fees. I thank Michael Schwabe for sharing the Toyota Memo and Pete Prossen for the sample Statement of Facts with me after I asked on the RAV4 EV mailing list for such help.)

In contrast, Magnussen Toyota of Palo Alto routinely files the correct paperwork for their RAV4 EV customers and has even helped customers of other dealers to make the corrections. That's going the extra mile and earning respect, loyalty, and probably more future customers. As an aside, all of my dealings with Magnussen have been positive, including getting my MR2 serviced there, buying parts, and going for test drives. Others report similar positive experiences about them.

To clarify things slightly, the dealer DMV clerk prepares the papers. The owner still needs to sign and send the papers to the DMV, usually with the registration payment to drive the processing along. But the dealer DMV clerk, being vastly more experienced filling out DMV paperwork than the average civilian, is far better able to do this for a customer.

With that aggravation, we were agitated enough to bear waiting in line at the DMV for an hour to make the corrections ourselves. We made this first pass on October 31, 2003, Halloween Eve. An initial stop at the AAA DMV window revealed that they didn't know how to make this happen in the DMV end, though in principle it should have been the same as any other Statement of Facts to adjust car value, etc. (By the way, if you belong to your AAA affiliated auto club, you may find their DMV window to be much friendlier and more efficient than the state government DMV offices at least for routine things like paying your registration fees, etc.)

Here is a description of what we had to do to make it happen.

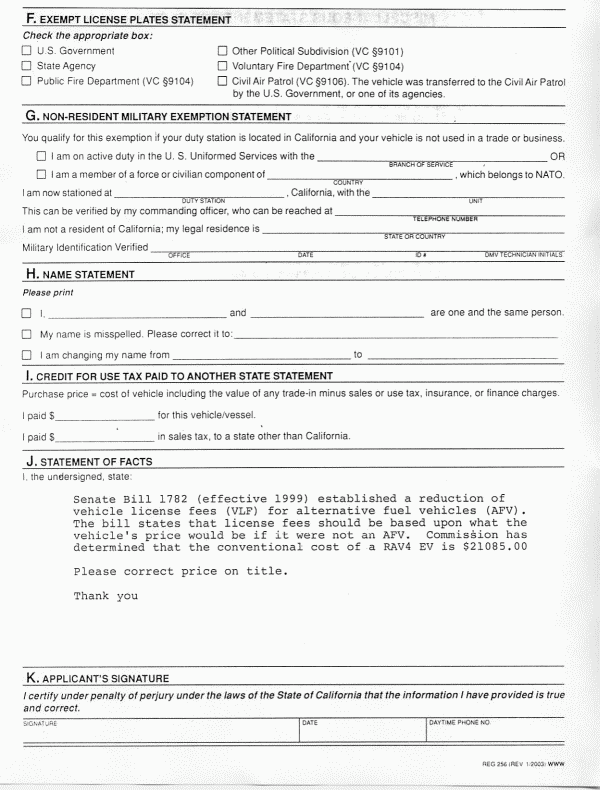

Senate Bill 1782 (effective 1999) established a reduction of vehicle license fees (VLF) for alternative fuel vehicles (AFV). The bill states that license fees should be based upon what the vehicle's price would be if it were not an AFV. Commission has determined that the conventional cost of a RAV4 EV is $21085.00Please correct price on title.

Thank you

Plugging $380 and $418 into the VLF offset fee calculator on the DMV web site shows our AFV reduced total fees for 2004 should have been $161. $418 - 161 = 257, which matches 256.50 rounded up. So we should expect an automatic check for $257 for the VLF offset restoration (repeal of the car tax).

Remember that in bureaucrateese, the Vehicle License Fee (which is based on car valuations) and the Registration Fee (which I believe is a fixed amount) are separate fees both included in your yearly fees. Looks like there's a county and local fee also.

Unfortunately the first year registration only shows the total amount, not a breakdown of VLF vs. registration fee portions, so it looks like I'll need to call the dealer for a breakdown of those two fees to come up with the correct revised number for last year's fees. Maybe our dealer will be able to help with that, or it's time to compare notes with Christine over at Toyota of Palo Alto.

November 3, 2003 I picked up the packet of info that the had DMV collected from us and took it to the dealer. After putting the DMV manager on the phone with the Toyota dealer DMV clerk, they decided that the dealer clerk should fill out a fresh statement of facts with the same info we used (i.e. the paragraph above), but sign and stamp it as the dealer.

I would then take the same packet back to the DMV and hand it to the manager, with the statement of facts that the dealer filled out and signed instead of us. That should be acceptable to DMV headquarters.

While at the dealer I asked the clerk to look up what the 2002 first year Vehicle License Fees should have been on $21,085. This will be needed to fill out the Application for Refund as mentioned above.

It appears that the Manufacturer's Suggested Retail Price (MSRP) should be used to subtract the incremental cost from, especially if the car was bought at the retail price which is usually the case for EVs. According to the text of the law, the incremental cost is a maximum and can be reduced by the actual purchase price, i.e. if the AFV were purchased for less than the retail price. (This is uncommon.)

"This determination shall constitute the maximum incremental cost for purposes of the exemption in subdivision (a), and may be reduced by the actual sales price of the vehicle. "

The law created by SB 1782 also says that the incremental cost should not be taxed, so we should probably be applying for a refund on the sales tax paid. The sales tax on $21,395 is not inconsequential at nearly $2000, so this is probably worth doing.

"the incremental... cost between an alternative fuel vehicle and a comparable conventional fuel vehicle, as determined by the State Energy Resources Conservation and Development Commission, should be exempt from both the vehicle license fee, and state and local sales and use taxes."I am contacting our dealer, Stevens Creek Toyota, to see if they can help with this. If not, we will go to Toyota of Palo Alto, which probably deserved our business in the first place since they seem more helpful.

Note that this is separate from the refund for the 2004 fees which everyone who paid in October and part of November 2003 was charged before Governor Schwarzenegger restored the 67.5% VLF offset ("repealing the car tax") upon taking office. We, along with other Californians who paid the increased fees should be getting a refund check from the state. In our case, 67.5% of the $380 VLF portion of the $418 total fees we paid for 2004 is $257, rounded up. The calculation is near the top of this document.

So in addition to the $140 we should get back as a result of straightening out the first year fees under the AFV adjustment, we should get a separate check for $257 of the second year 2004 fees under the recently restored VLF offset. The latter applies to anyone who paid their registration October 1 through mid-November 2003.

Assuming the VLF offset holds up intact, our future total fees should be less than $161 a year given depreciation. (VLF fees for every car reduce every year as its value decreases due to depreciation. This is taken into account automatically for everyones' VLF, based on the age of the car.)

State Board of EqualizationIf the process needs to be done by the car dealer, then the board will send the letter back to us indicating that.

450 N Street

MIC: 37

P.O. Box 942879

Sacramento, CA 94279-0037

Here is a draft of our letter to the Board of Equalization requesting a refund and stating our reasons for the request. I am not an attorney; this is simply my best guess at language that might work.

"The sales tax exemption you mentioned under SB 1782 was not available during January 1, 1999 through December 31, 2002. The exemption only applied to vehicle license fees. There appears to be no other grounds for your Claim.... If the seller (the dealer) does decide to file a Claim for Refund on your behalf, we will recommend to the Board that the Claim be denied for the reasons stated above."Has anyone been able to get a refund on the sales tax paid on the incremental cost of the AFV?

It seems there's a major disconnect in SB 1782 between the stated intent of the legislature, which is clearly to reduce VLF and state and local sales and use taxes:

(From SECTION 1.:)and what they actually implemented, which only seems to mention VLF:(i) It is the intent of the Legislature to equalize the vehicle license fee, and state and local sales and use taxes, between alternative fuel vehicles and conventional fuel vehicles for a period of four years, beginning January 1, 1999, and ending December 31, 2002. During this time period it is the intent of the Legislature that the incremental or differential cost between an alternative fuel vehicle and a comparable conventional fuel vehicle, as determined by the State Energy Resources Conservation and Development Commission, should be exempt from both the vehicle license fee, and state and local sales and use taxes.

(From LEGISLATIVE COUNSEL'S DIGEST preamble:)and:This bill would, until January 1, 2003, for purposes of determining the vehicle license fee, exempt from the determination of market value, the incremental costs, as defined, that are incurred with respect to a new light-duty motor vehicle propelled by an alternative fuel that is certified by the State Air Resources Board as producing emissions that meet, or are lower than, the emission standards and other specifications for ultra-low-emission vehicles, as defined by the board.

SEC. 2. Section 10759.5 is added to the Revenue and Taxation Code, to read:It seems the actual modifications to the code only mention VLF. Am I reading this disparity between legislative intent and action correctly? Here's a response from Darell Dickey confirming that he got similar results:10759.5. (a) For purposes of determining the vehicle license fee imposed by this part, there are exempted from the determination of market value, the incremental costs of new light-duty motor vehicles propelled by alternative fuels, and certified by the State Air Resources Board as producing emissions that meet the emission standard for ultra-low-emission vehicles or lower as defined by the board. This exemption shall apply to the subsequent payments of the vehicle license fee.

On Friday, April 30, 2004, 4:47:21 PM, Darell Dickey wrote:And here's another similar response from Dave Modisette:I spent quite a bit of effort on this myself, and came to the same conclusion you have. In fact, you asked and answered your own question below. [above] Even though the tax portion was *intended* to be reduced along with the registration, it was never implemented. And only the implemented part counts for anything.

On Monday, May 3, 2004, 9:54:33 AM, Dave Modisette wrote:I think I can answer your questions, but it is not good news. There is no incremental exemption from the sales tax, only the VLF.

There is a disconnect between the intent language of SB 1782 and the codified statute (Rev & Tax 10759.5). This is because the first (as introduced) version of the bill contained both the sales tax exemption and the VLF exemption. But the first legislative committee removed the sales tax exemption right away, leaving only the VLF exemption. Reason: sales tax exemption takes revenue away from state government, while VLF takes (or used to take) revenues away from local governments; legislators didn't want to reduce their own revenues, only the revenues of local officials. The legislative committee that took out the sales tax exemption didn't correct the intent language, which is sloppy drafting.

It does look like the 2002 legislation extending the exemption (AB 2461) until 1/1/2009 corrected the intent language. It looks like it only refers to the VLF exemption now.

Other incentives, such as state grants, for AFVs were extended through Spring of 2003 mainly to accommodate the final few remaining Toyota RAV4 EV purchases after December 31, 2002. And according to Dave Modisette above, 2002's AB 2461 extends the VLF reduction for AVFs until 1/1/2009, so future AFVs should get the incremental cost VLF reduction for several years to come. This will continue a good savings to future EV and other AFV operators. The Federal Income tax deduction is possibly being phased out over time.

All the DMV forms are available on the DMV website.

{kind=link}

{kind=link}

{kind=link}